Assets are anything of value that your business owns. Even the smallest business has assets, which can include everything from cash in the bank, to the computer you’re working on, to the building where you manufacture piggy banks. If it has value, it’s considered an asset.

A business can have a variety of assets including:

You are viewing: Which Of The Following Is Classified As A Plant Asset

- Current assets

- Investments (long-term)

- Fixed assets

- Intangible assets

Plant assets, also known as fixed assets, are any asset directly involved in revenue generation with a useful life greater than one year. Named during the industrial revolution, plant assets are no longer limited to factory or manufacturing equipment but also include any asset used in revenue production.

The best way to manage your assets is to use an accounting software application that simplifies the entire asset management process from the initial acquisition to asset disposal.

Overview: What are plant assets?

Plant assets are long-term assets directly used in revenue production. Plant assets always have a useful life greater than one year, and they’re generally used in revenue production daily. There are five main categories of plant assets, with most plant assets falling under one category:

- Office equipment

- Plant equipment and machinery

- Buildings

- Land

- Improvements

There are five major plant asset categories that you may use in your business. Image source: Author

Because plant assets have a useful life greater than a year, their expense is not recorded during purchase, but should be depreciated over the useful life of the asset, keeping the purchase consistent with the matching principle which states that expenses should be recorded when they can be matched with generated revenue.

The only exception is land, which does not have a limited useful life, so cannot be depreciated.

When depreciating plant assets, use the entire cost of plant assets when calculating depreciation. To depreciate machinery and equipment, you can use the following depreciation methods:

- Straight line method: Straight line depreciation is the easiest depreciation method, with the same depreciation expense recorded yearly. For example, if you purchase a piece of equipment for $15,000, with a useful life of three years, your depreciation expense would be $5,000 annually, not including salvage cost.

- Double declining balance method: Best used for vehicles and other items that lose value more rapidly in the first few years of use, double declining depreciation is an accelerated depreciation method that depreciates asset value at double the straight line method. Unlike straight line depreciation, double declining depreciation expense changes from year to year, with the first two years the highest, and with depreciation expense declining in subsequent years.

- Units of production method: The units of production depreciation method can be used for equipment whose useful life is based on production levels rather than years of use. You can depreciate equipment based on hours of use or output, depending on the machine and its use.

Read more : Which Of These Would Not Decrease Basis

As for buildings, per IRS rules, non-residential buildings can be depreciated over 39 years using the Modified Accelerated Cost Recovery System (MACRS) method of depreciation.

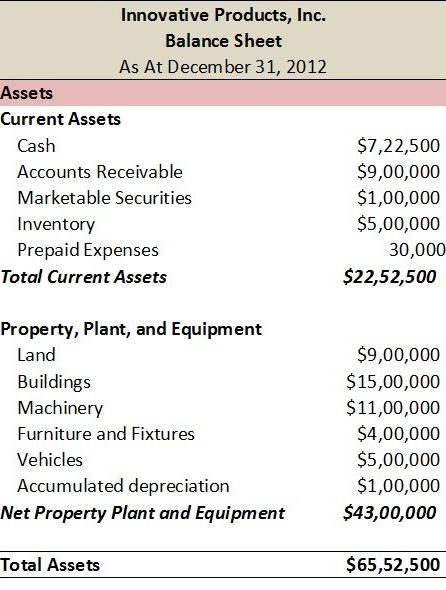

Plant assets, like all assets, are reported on your balance sheet, where they are typically displayed separately from current assets and are usually listed as fixed assets, long-term assets or property, and plant and equipment (PP&E) assets.

Property, Plant, and Equipment Assets are categorized separately on a balance sheet. Image source: Author

Common examples of plant assets

Using the five major plant asset categories, the following are examples of plant assets:

- Machinery: Press brakes, beveling machines, and band saws are examples of machinery.

- Equipment: Die casting machines, production machines, foundry equipment, and edge-banding machines are examples of equipment.

- Construction: Building construction is considered a plant asset.

- Renovations: An addition to an existing facility or the renovation of a building would be considered a plant asset.

- Office equipment: Desktop computers, laptops, copiers, and printers are all plant assets.

- Vehicles: Delivery vehicles and trucks for hauling equipment would be considered a plant asset.

- Furniture and fixtures: Furniture such as office desks, workstations, tables, chairs, and lighting fixtures are all plant assets.

- Facilities: the building that houses your business or manufacturing plant are plant assets.

- Land: Any land that your business owns is considered a plant asset. Remember land is the only plant asset that should not be depreciated.

- Land maintenance: Land improvements are also considered a plant asset, and sometimes are considered depreciable, if the improvement has a useful life, like erecting a fence.

What characteristics do plant assets have in common?

Some major characteristics all plant assets share:

- They are used directly in operations or revenue generation.

- They have a useful life longer than one year.

- They are tangible, meaning they have a physical presence.

- They are usually, except for land, subject to depreciation.

Source: https://t-tees.com

Category: WHICH